Is the US in recession?

It depends on whom you ask...

The US GDP figures landed for Q2: GDP fell 0.9%. GDP also fell 1.6% in Q1. This has triggered a significant amount of discussion about whether the US is in a recession or what a recession even is.

The White House pre-emptively argued that a recession takes more than two consecutive quarters of negative GDP growth. In some ways, the White House is correct. In the US, ‘people’ agree that the NBER decleares whether a period is a recession. The declaration is based on whether there is a broad economic slow down, rather than merely a decline in GDP.

But this is question begging: How exactly does the NBER define a recession? Who gave the NBER authority and why? And, why is the NBER’s definition or declaration the right one? Why is the NBER’s view ‘more correct’ than the standard definition that a technical recession involves two quarters of negative GDP growth?

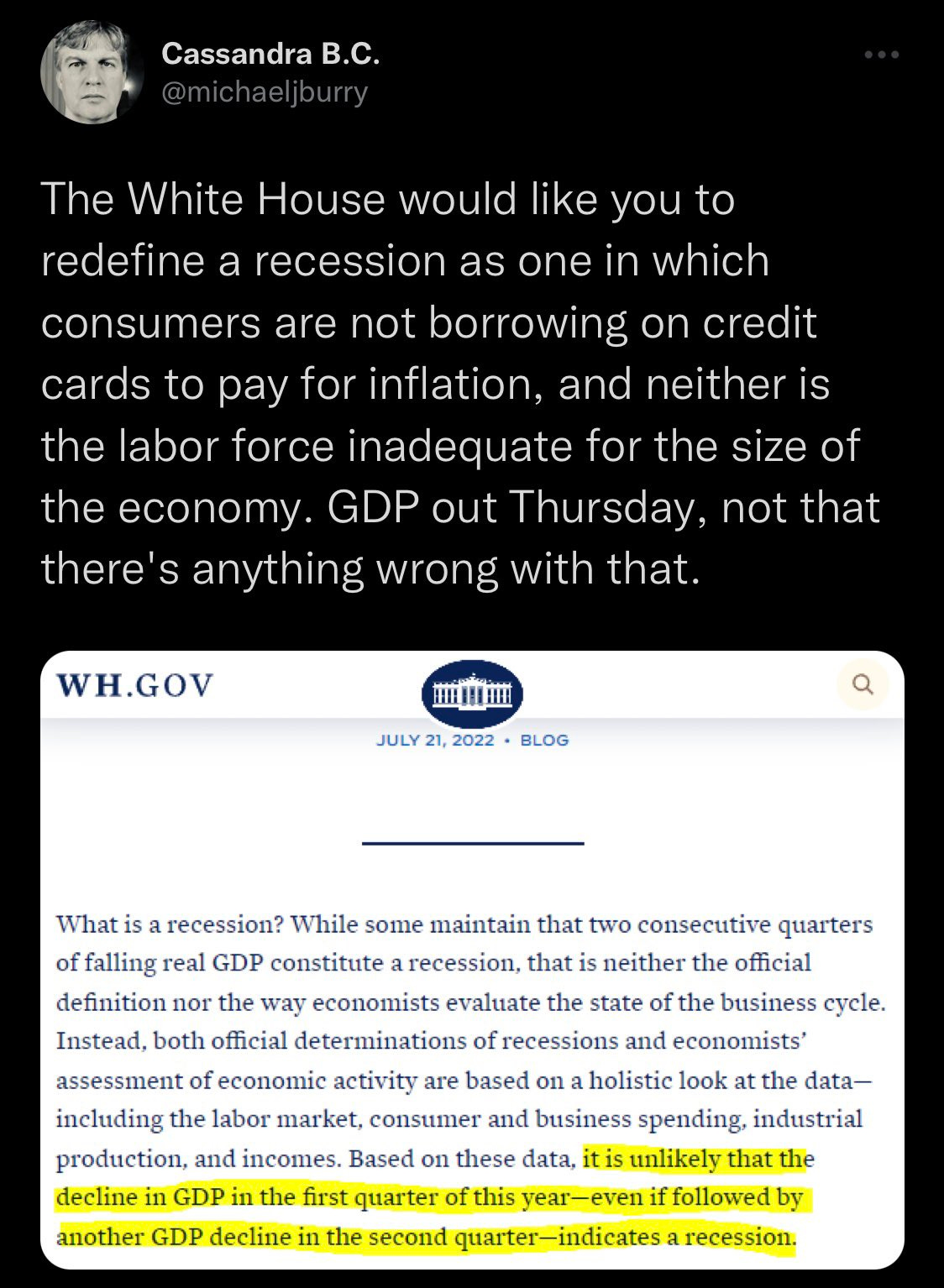

This means that whether something is magically labelled a ‘recession’ is besides the point. The issue is whether the economy is doing badly. Michael Burry highlighted this in a tweet soon before the GDP data landed.

But is Michael Burry correct? Or is the White House correct? What does the data tell us? The short answer is that the GDP data was not good. There was a broad based slow down in many areas, especially on goods based expenditure. And, there are reasons to think this could worsen.

Indeed, the yield curve has become even more inverted, suggesting heighted recession risk. However, strangely, corporate earnings expectations seem not to fully reflect some of this downside: corporate earnings continue to disappoint, suggesting there coudl be further equity downside.

Given the myriad factors influencing the economic outlook, the below video discusses them in detail.