Michael Burry shorts the market!

Michael Burry’s latest 13F filing reveals several interesting positions. One of the more pertinent is the put options over two index ETFs: SPY and QQQ. SPY follows the S&P500. QQQ follows the NASDAQ composite. Michael Burry’s positions suggest that he believes the market will fall. But, it is not clear that this position has been profitable or that it will become so.

Let us analyze Michael Burry’s positions. Further, premium subscribers can get access to analyst consensus forecasts for the S&P500 and ASX200 below (all the way at the end).

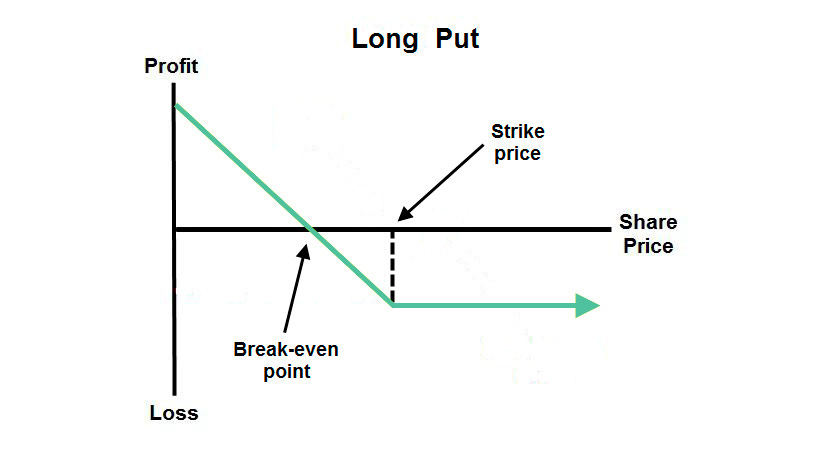

The put options give Michael Burry the right, but not the obligation, to sell the underlying ETFs at a predetermined strike price at a predetermined date. A put option holder benefits if the stock price falls. Intuitively, if the strike price is $100 but the underlying asset falls to $90, the holder could buy the asset in the market for $90 and sell it using the option for $100, pocketing $10. In exchange for this right, the option buyer must pay an option premium (i.e., the price per option). Importantly, the put option holder need not exercise their right, meaning that the payoff is the maximum of the strike price less the end price, or zero. The profit is the payoff less the option premium.

We do not have full details on Michael Burry’s options. We do not know the strike price, expiry date, or what he paid. Therefore, we do not know for sure whether he has gained or lost on the positions or under what conditions he will gain or lose. However, given that the market has risen since June 30, it is likely he has lost money on the position if he still holds it.

Michael Burry’s put options signal bearishness about the broader market. This could belie several things:

1. A belief that the market is overpriced. This might flow from the P/E ratio (and forward P/E ratio) being above the five and 10 year averages. It also quadrates with the market remaining persistently string despite S&P500 earnings declining.

2. Perceptions that the market has not priced-in a recession when it should have. This belief might reflect Michael Burry’s prior statements that the Fed might keep rates too high for too long, triggering a downturn.

3. An attempt to hedge market risk inherent in other long positions and an attempt to capture the alpha from those positions alone.

Michael Burry might well have lost money on these positions. He entered them in 2023 Q2. However, the market increased during this time. Thus, the put options would have fallen in value. Depending on when they expire, these positions could ultimately expire worthless, potentially being extremely costly. The market has increased since June 30. And, we do not know the strike price or when he bought the options. Thus, we do not have enough information to say whether the position has been profitable.