Michael Burry warns stocks have further to fall

Think twice before buying the dip

Michael Burry has issued another bearish warning. This time he has specifically focused on corporate earnings. He has raised the prospect of declining earnings compounding an already significant decline in valuations.

But, have valuations really fallen? And, will earnings follow suit?

What has happened to valuations?

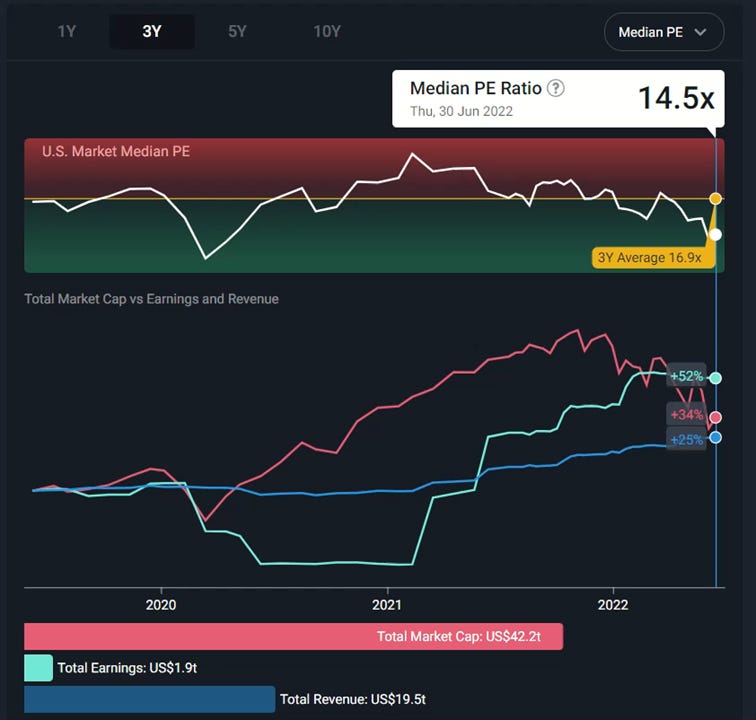

Michael Burry has noted that there has been “multiple compression”. He appears to be referring to market price-to-earnings (i.e., P/E) multiples falling. This is accurate. According to Simply Wall St, the median P/E ratio has fallen to 14.5x. The decline has mainly been due to a fall in valuations rather than in present earnings per se.

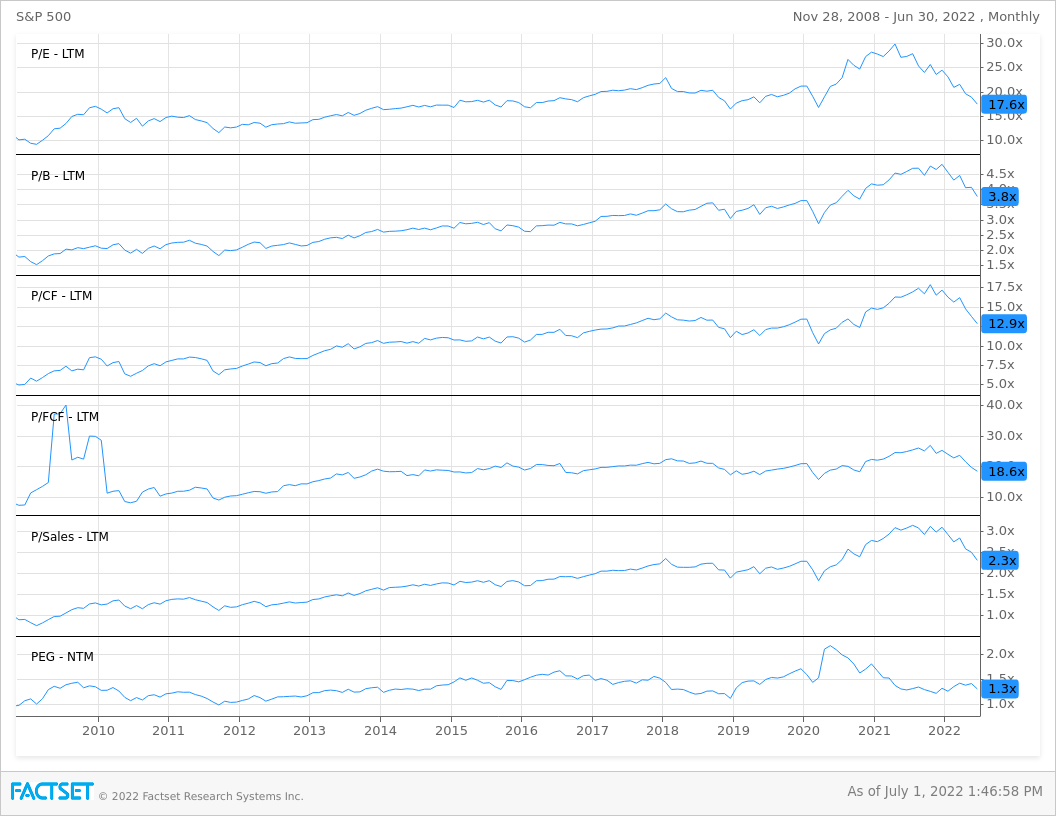

Many multiples have decreased. This includes both the mean and median P/E ratios. It also includes other ratios, such as price-to-sales and price-to-book. It is also consistent across data providers. For example, Factset shows a significant decline across several multiples from firms’ highs in 2021.

These declines are important. The firm’s share price is the present value of all future earnings. Ideally, the valuer can determine this via a discounted cash flow valuation. However, analysts can approximate it by using market-wide P/E ratios. Here, the approximate value would be:

Estimated Price = (Market Wide P/E) x Earnings

Therefore, if the market wide P/E declines, the estimated price for each firm will decline. Thus, the Michael Burry’s first proposition, that multiples have fallen is clearly correct.

What about earnings?

Michael Burry has indicated that earnings might fall and the market has not fully priced in such a fall. This implies a further reduction in company valuations. This is a forward-looking statement. Thus, it is impossible to know whether earnings will fall. However, we can assess whether it is a significant risk.

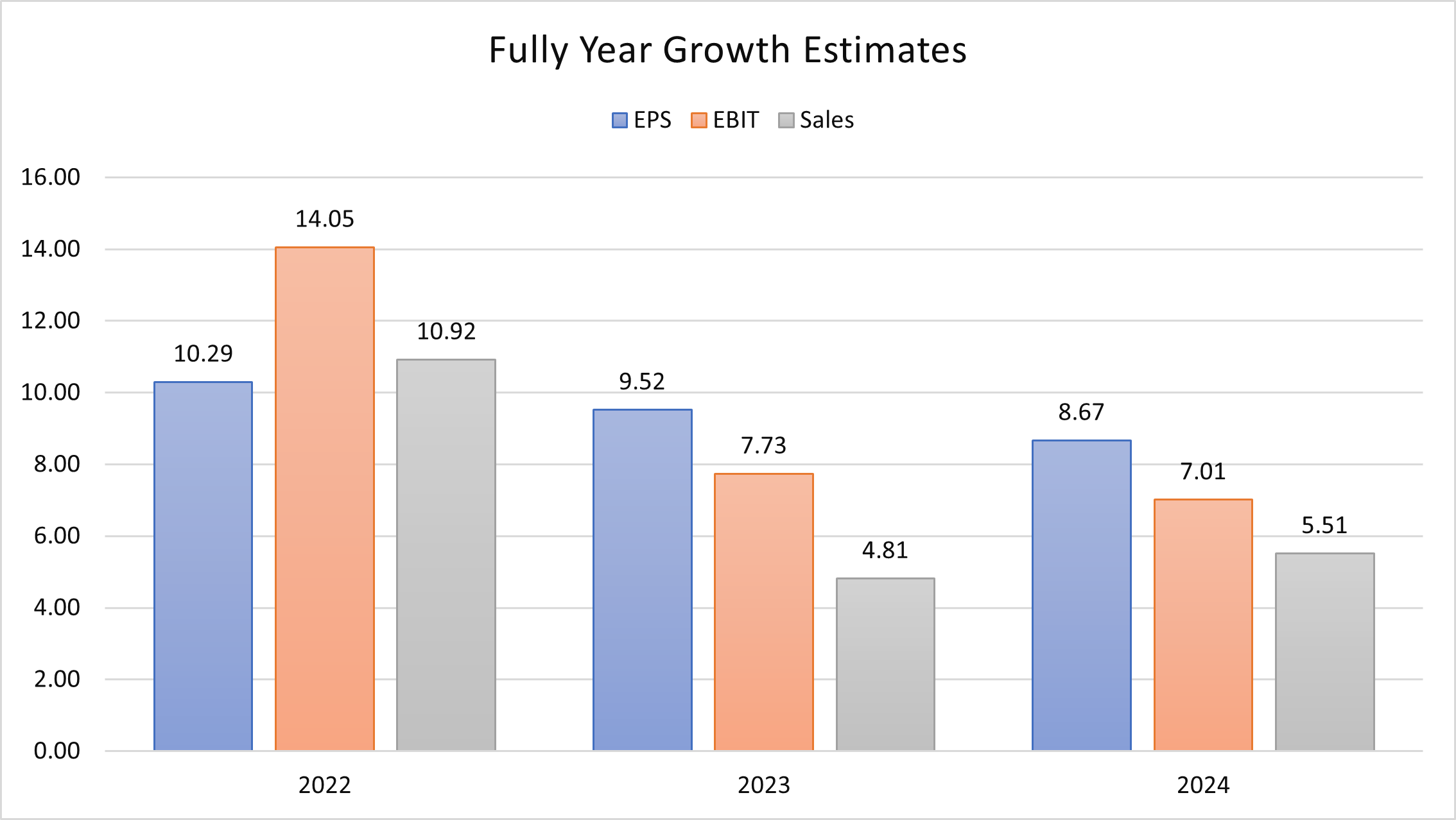

We must start by analyzing what earnings the market currently expects; and thus, what the market has priced in. According to Factset, the market expects EPS to growth around 10.3% during 2022, on average. Simply Wall St reports similar numbers.

The question is then whether factors could cause earnings to fall and/or to disappoint. Here, we see several issues. These influence firms’ top line revenues and bottom line earnings.

Revenues could fall and could under-perform the 10.92% sales growth that analysts predict. The headwinds vary between industry. However, the Federal Reserve expects declining GDP growth (and for GDP growth to be under 2% in 2022). They also expect to increase policy interest rates to around 3.8% in 2023. Indeed, 30-year mortgage rates already are near 6%. This reduces consumer spending power. This manifests in a worsening outlook in myriad sectors. For example, retailers have reported an inventory build up, declining interest coverage ratio, and the risk of having to discount goods in the second half of 2022.

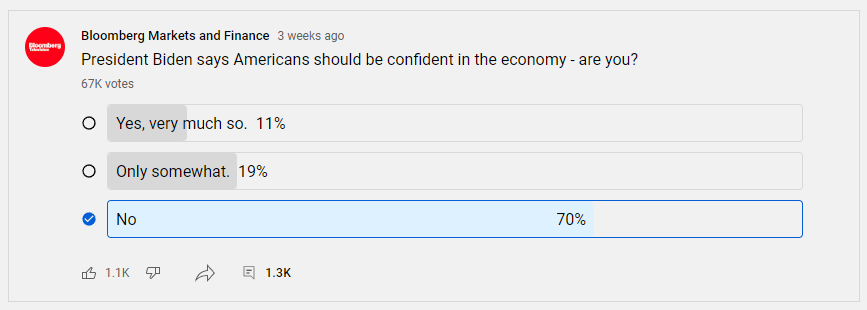

Consumer sentiment reflects these issues. Personal Consumption Expenditure is down in inflation-adjusted terms (cf. nominal terms). The University of Michigan consumer sentiment survey puts consumer sentiment at near record lows. Similarly, social media companies have reported declining revenues per user on declining advertisting revenue. This suggests worsening economic expectations. Bloomberg has also surveyed its YouTube viewers, with 70% of 67,000 respondents indicating a lack of confidence in the economy.

Firms also face increasing expenses. Inflation has pushed wages and the cost of goods higher. Retailers seem to facing limits to how much they can pass this on to consumers. Further, rising rates increase firms’ cost of capital. Thus, there is a hit to many firms’ bottom line.

Michael Burry is not alone in expressing these concerns. BlackRock has similarly stated: “We expect the energy crunch to hit growth and higher labor costs to eat into profits. The problem: Consensus earnings estimates don’t appear to reflect this”. Further, BlackRock has flagged recessionary risks, highlighting “The risk has risen that central banks slam the policy brakes as they focus solely on inflation without fully acknowledging the high costs to growth and jobs”. Thus, other major investors appear to be reticent to ‘buy the dip’ as stock prices decline.

What then for investment?

Michael Burry’s bearish prediction does not leave much rooom for equity investment. Indeed, if stock prices are expected to fall, then one would consider holding cash until at least some of the earnings declines have impacted prices. That is, if earnings are expected to fall, investors could sit out the market until firms do announce their disappointing earnings. Investors can then reconsider whether to invest.

If investors wish to remain invested in such a market, it would appear best to do detailed fundamental analysis. Rather than investing in broad sectors, industries, or markets, investors would need to consider the individual characteristics of individual stocks. This would involve analyzing how individual firms’ growth rates might compare to what analysts have priced in. And, investors would then need to hunt for companies trading at ‘margin of safety prices’. Investors might do this using valuation tools such as in Simply Wall St.

When looking at individual companies’ details, investors should consider factors including: (1) What is the firm’s capital structure? Will it suffer as rates rise. (2) Does the firm have pricing power vis-a-vis customers? Can it pass on rising costs to customers? (3) Can the firm resist rising costs from suppliers? Does it have a dominant or market leading position in relation to them? (4) How has the market priced the firm? Has the market excessively ‘penalized’ the firm based on falling markets? Has the sector become so popular that everyone has rushed into investing in it, driving prices excessively high.