RBA Rate Cut Explained and Explored

Relief at last?

The RBA has cut rates by 25bps in one of its more controversial interest rate decisions. The decision was controversial partly due to the political stakes involved and the appearance of political pressure. However, it was also controversial because underlying inflation remains above the RBA’s 2-3% target.

The RBA’s stated reason for cutting rates is:

“In the December quarter underlying inflation was 3.2 per cent, which suggests inflationary pressures are easing a little more quickly than expected. There has also been continued subdued growth in private demand and wage pressures have eased. These factors give the Board more confidence that inflation is moving sustainably towards the midpoint of the 2–3 per cent target range.”

The RBA’s stated logic is curious, however. The RBA ideally aims to get underlying inflation towards the midpoint of its target range (i.e. 2.5%). However, the RBA’s own forecasts suggest that the proxy for underlying inflation is expected to remain above 2.5% throughout its target period. Furthermore, the RBA stated:

“The forecasts published today suggest that, if monetary policy is eased too much too soon, disinflation could stall, and inflation would settle above the midpoint of the target range. In removing a little of the policy restrictiveness in its decision today, the Board acknowledges that progress has been made but is cautious about the outlook.”

We can start with the political pressure. The ruling Australian Labor party has been suffering in the polls, with a strong possibility that they will lose seats in the House of Representatives and be unable to form majority government. Thus, there are reports that members of parliament were calling for the RBA to cut rates. Political pressure is unlikely to cause a rate cut if it were not already a possibility. However, in a close decision, a rational agent might err on the side of reducing political blowback. Unfortunately for the RBA, the appearance of political influence opens the RBA to criticism.

The RBA faces a further conundrum. Inflation remains high due to government spending. This is clear from the factors that contribute to Australian GDP growth: Government spending is offsetting a faltering private sector. However, such spending is myopic as it increases inflation. In response to the inflation and interest rates, the Government has enacted subsidies, which tautologically involve more spending. These subsidies temporarily reduce price growth and headline inflation. The RBA sees through this charade but the federal government can falsely claim that it has reduced inflation. The net result is that government spending exacerbates underlying inflation even if it temporarily reduces headline inflation, which triggers elevated interest rates, which triggers more government spending, which keeps rates higher for longer. But, unfortunately, the people impacted by the higher rates do not receive the subsidies in a proportionate manner. Thus, those on the receiving end of the higher rates ultimately bear the cost of bad fiscal policy.

A further wrinkle is labor productivity. The RBA has noted that poor labor productivity risks exacerbating inflation. That is, if productivity increases, then (in simple terms) it costs less to produce the same amount of output. By contrast, if productivity falls, it costs more. In Australia, GDP per hour worked – the estimate of productivity – fell 0.8% y/y in the latest release (Q3, 2024). The RBA also suggests hat it will fall leading to June 2025.

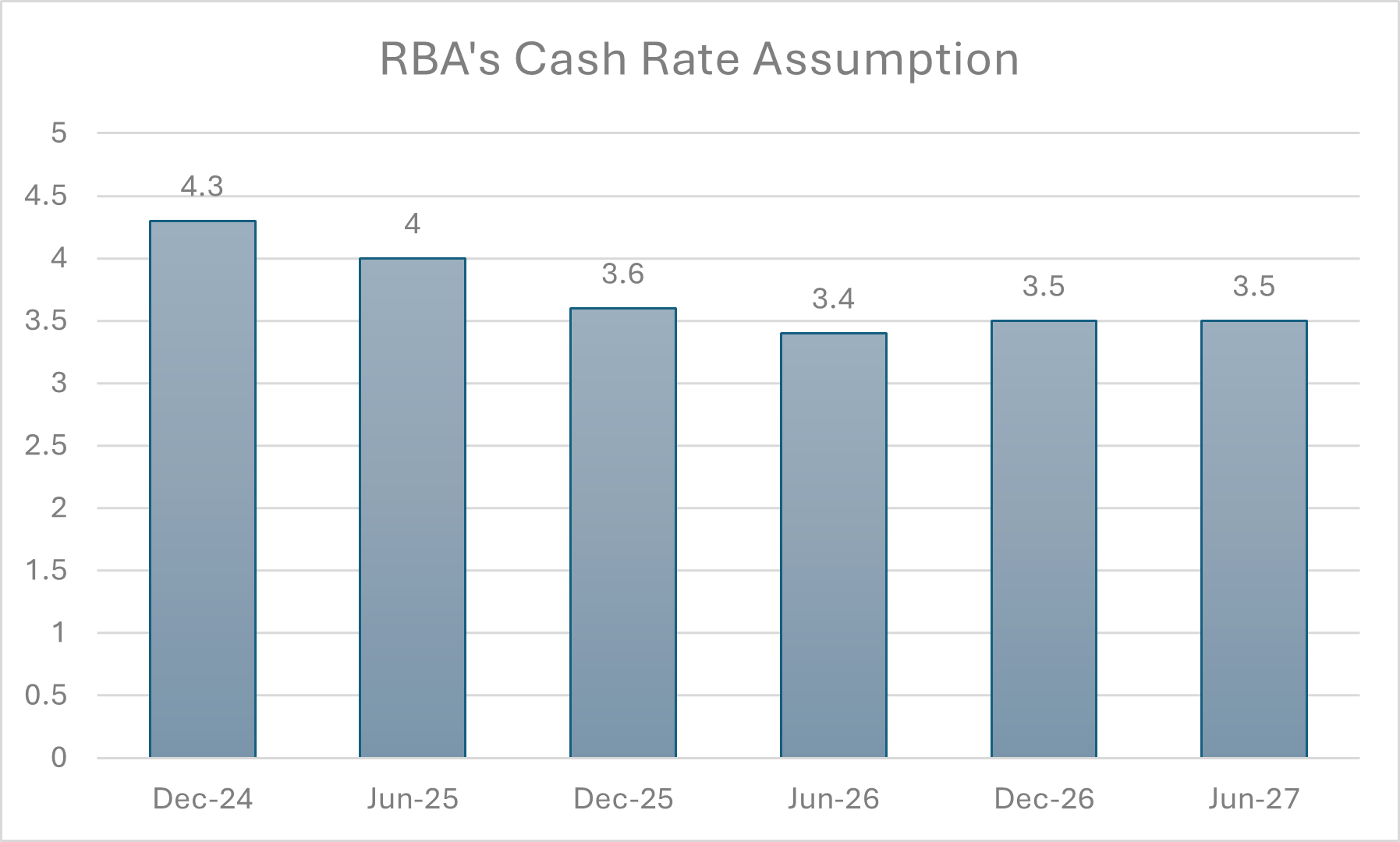

Going forward, it is uncertain whether and when underlying will approach the RBA’s target. The RBA forecasts underlying (i.e., trimmed mean) inflation to remain at least 2.7% during their forecast period. However, the RBA also suggests that the cash rate could approach 3.6% by December 2025. Whether this is realistic or wishful thinking could depend on whether governments can restrain their election spending and fiscal stimulus during the election campaign.