Why export taxes will backfire

When increasing tax rates reduces tax revenue

Oil and gas prices have soared in the wake of the Iran conflict. Domestic supply has come under pressure. Predictably, talk has turned to whether to impose a “windfall” tax on gas exports, with a parliamentary select committee formed to investigate.

Some politicians, such as Senator David Pocock, have called for a 25% tax on gas exports. However, commodities companies, and the Business Council of Australia, have warned that such an export tax would jeopardize Australia’s supply, and raise little – if any – revenue.

So which is it? Well, it turns out that when you model the impact of an export tax, the results are profoundly negative.

The intuition is straightforward an export tax renders marginal production uneconomic and deters exploration. Oil and gas production curves are stepped. This means that we have different types of production, with different cost bases. And, only so much supply is available at cheap prices. For example, we might have cheap onshore, expensive offshore, and unconventional production. If the price received consistently falls below the breakeven point for a production type, it will cease.

The impact of an export tax is therefore obvious: where the export tax reduces the price received below the breakeven point for a technology, that technology simply stops being utilized. In so doing, it reduces (or eliminates) exports, causing the export tax to raise less revenue than claimed. Furthermore, by reducing production and corporate profits, corporate income tax falls. Most gas companies do indeed pay export taxes. For example, Santos’s tax rate was around 22% of its gross profits (cf Net Income), and 31% of its profits before tax.

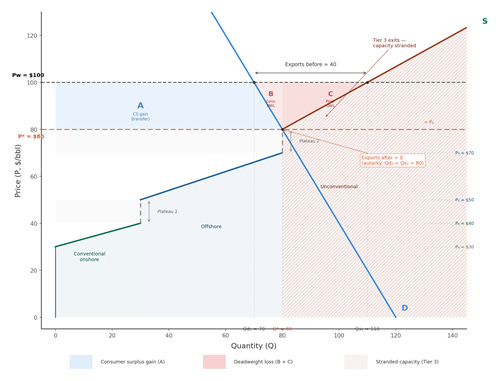

Let’s use oil prices, to which natural gas is largely benchmarked, for clarity of discussion. Oil prices are a convenient benchmark because they are relatively standardized across countries. So, in round numbers, ‘cheap’ production might be viable at a price of USD 30/barrel, mid-tier production viable at a price of USD 50, and expensive production at a price of USD 80. Clearly, the expensive production would be difficult to get off the ground as world oil prices frequently dip below USD 80/barrel, even if they are currently hovering near USD 100. The problem is obvious, if there is a 25% export tax, then the price received will be too low to justify ‘expensive’ production types. This tautologically limits the amount of oil that would be produce. The logic applies mutatis mutandis to gas or any other commodity. An example of what this might look like is below.

Figure 1: Supply and Demand, and welfare effects of a 25% export tax. The stepped supply curve reflects three production tiers with breakeven prices at $30, $50, and $80/bbl. Before the tax, the world price of $100 supports 110 units of supply, 70 of domestic demand, and 40 units of exports. The export tax drives the domestic price to $80 (the autarky equilibrium), eliminating Tier 3, contracting supply to 80, and absorbing all output domestically. Area A represents the consumer surplus gain; areas B and C represent consumption and production deadweight loss respectively. The hatched region denotes stranded Tier 3 capacity.

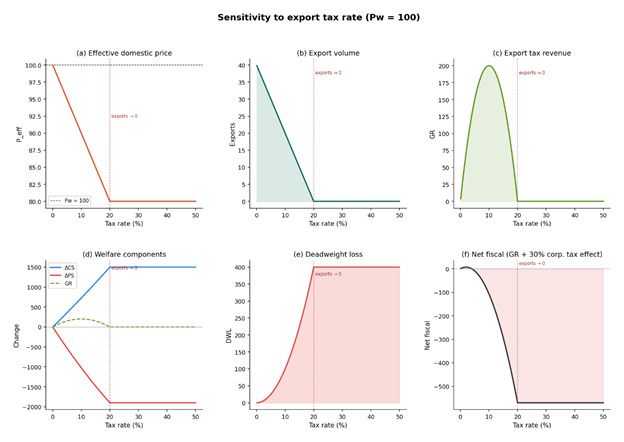

Because export taxes significantly alter potential supply, it turns out that the optimal export tax rate is in single digits. But, only if we ignore the inherent risk and volatility associated with commodities and the negative signal an export tax sends to businesses. For example, using a partial equilibrium model, we find the below ‘fiscal Laffer curve’, with export tax revenue being optimized at an export tax rate of around 10%, but total net revenue being maximized at an export tax rate of around 4%. Indeed, depending on production quantities, an export tax can indeed eliminate exports, which causes the export tax to raise precisely zero revenue.

Figure 2: Export tax sensitivity: Each panel shows the response of a key variable to export tax rates from 0% to 50%, holding the world price at $100/barrel and the corporate tax rate at 30%. The vertical dashed line marks the export-killing threshold ( 20%), beyond which the economy enters autarky. Panel (a): effective domestic price. Panel (b): export volume. Panel (c): export tax revenue, which peaks at approximately T= 10%. Panel (d): changes in consumer surplus, producer surplus, and export tax revenue. Panel (e): deadweight loss. Panel (f): net fiscal position (export tax revenue plus change in corporate tax receipts), which turns negative at approximately T= 4%.

To be clear, the optimal level can depend on the presumed elasticity of demand and the quantity available at each production tier. However, what is clear, is that an export tax of 25% does reduce production because it renders ‘expensive’ production technologies and exploration uneconomic.

And this is not to mention risk: commodities are notoriously volatile. Commodities companies rely on upmarkets to offset downmarkets. Remove the upside through “windfall taxes”, and the expected price received will fall. Tautologically, production will fall as higher marginal cost production is discarded.

But it gets worse. The “windfall export taxes” also send a very negative signal to successful companies: you take the risk and the government takes the rewards. Once the government sends a signal that it will impose ex post tax changes that render capex unprofitable, business will rightly scale back production. This shrinks the pie and reduces the tax base.

Myriad spurious claims about export taxes abound. The most disingenuous of which is to compare Australia to Norway. Notably, in Norway, the government controls production, owing two thirds of the major gas producer. This means that that an export tax effectively shuffles money between government departments in Norway. Norway is irrelevant to Australia. It is also worth noting that Norway has a poor record with tax design, imposing wealth and export taxes, which undermine entrepreneurship.

A related spurious claim is that exports will keep flowing even if there is an export tax and that claims otherwise are scaremongering. However, as illustrated above, it is very clear that once a production tier is uneconomic, it will simply cease. This should be accounting and finance 101: it is basic arithmetic.

The net result: export taxes are a bad idea and should be avoided. It is not clear they will even raise money and they will certainly deter production and exploration. Instead of shrinking the pie by hiking taxes, the government should look to how to grow the pie, increase the tax base, and drive growth.